_______________

_______________

The real estate market took a big turn, with home values falling for nearly two years. Because of such an inconsistent landscape, borrowers have had to review their strategies. Although it can be seen as some good that comes from the house prices falling, other concerns must be taken into account before making any financial decision.

Understanding the Drop in Home Values

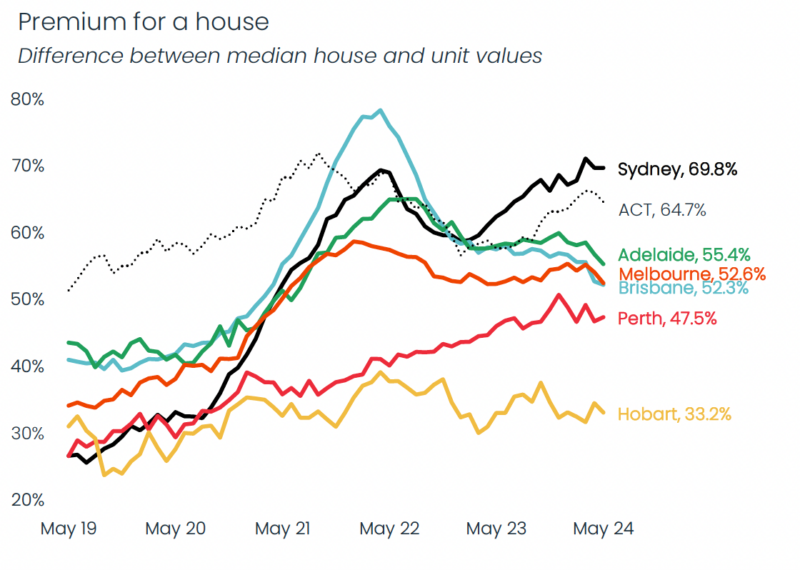

Premium for a House: Tracking the Gap Between Median House and Unit Values Across Australian Cities (May 2019 - May 2024)

A decrease in home values affects both buyers and existing homeowners. It might offer

prospects for potential buyers to engage in the market at reduced costs. However, declining prices may also imply a slowing down market, which is likely to affect prospective performance on investments even further.

For homeowners, decreased property values might change equity levels, thus leading to different refinancing options or alternatives to using home equity loans. This is why timing is important when thinking about any major financial decisions related to land ownership Key Points for Borrowers.

While borrowers should be more active to benefit from this change in the market, some important considerations are as follows:

For those who borrow money from banks, this alteration clearly shows how important changing strategies to match the market development patterns can be.

A Quick Look at Regional Performance

Melbourne reported a 3% decrease in values in 2024 compared to Hobart and ACT, which experienced declines of 0.6% and 0.4%, respectively.

Greatest Growth: Perth recorded an astonishing 19.1% increment in its prices, followed by Adelaide (13.1%) and Brisbane (11.2%).

Sydney: Despite modest growth of 2.3%, Sydney remains the most expensive city, with a median house price of $1,191,955, well above the national median of $814,837.

By the end of Q4-24 Adelaide had outperformed Perth as the best-performing market; this was due to a low level of sales activity on very few homes listed here as there were only 66 properties for sale through all Real Estate Agents in South Australia compared to the five-year average over this period at around 100 properties for sale (being about one third less than usual). On the other hand, growth in Perth slowed down by only increasing by 1.9 per cent because there was more supply, making more choices available to buyers.

Evaluate Borrowing Power

Typically, changes in property value lead to a shift in lending criteria. You could be affected by such things as lenders reviewing loan-to-value (LTV) ratios, which will determine how much you can borrow. For that reason, it is up to borrowers and their financial advisors to evaluate the current capacities.

What caused the shift?

This change happened because of several things, including higher interest rates, rising living costs, and a reduced ability to borrow. According to CoreLogic’s research director, Tim Lawless, it tells us that the market is still catching up with affordability issues and increased advertised supply.

The fact that real estate markets keep changing is evident from the decline in housing values today. Overcoming these challenges and transforming them into opportunities lies with borrowers who are informed and whose strategies match professional advice.

OM Financials assists borrowers in going through these changes using customized financial solutions.

Reach out to OM Financials now and let us help you on your way to financial freedom.

08 Jan 2025, 12:00 AM

05 Jan 2025, 12:00 AM

30 Dec 2024, 12:00 AM

28 Dec 2024, 12:00 AM

23 Dec 2024, 12:00 AM

At OM Financial Services, our experienced group of contract brokers can compare a wide extent of domestic credits over a board of 50+ banks. This means we won’t use any ancient arrangements for you. We will find the best current arrangement to meet your needs. Our fund masters are talented in taking care of advances, from domestic credit to individual credit, right through asset and commercial finance. We can assist you get advance pre-approval and can give master help for borrowers looking to renegotiate. With OM Financial Services, you’ll have access to comprehensive choices to help assist you with borrowing.