_______________

_______________

As Australia navigates the complexities of a high-interest-rate environment, the sustained growth in residential and commercial property lending bodes well for the economy. The resilience of borrowers and the stability of lending standards suggest that the housing market will remain a key driver of economic activity in the coming months.

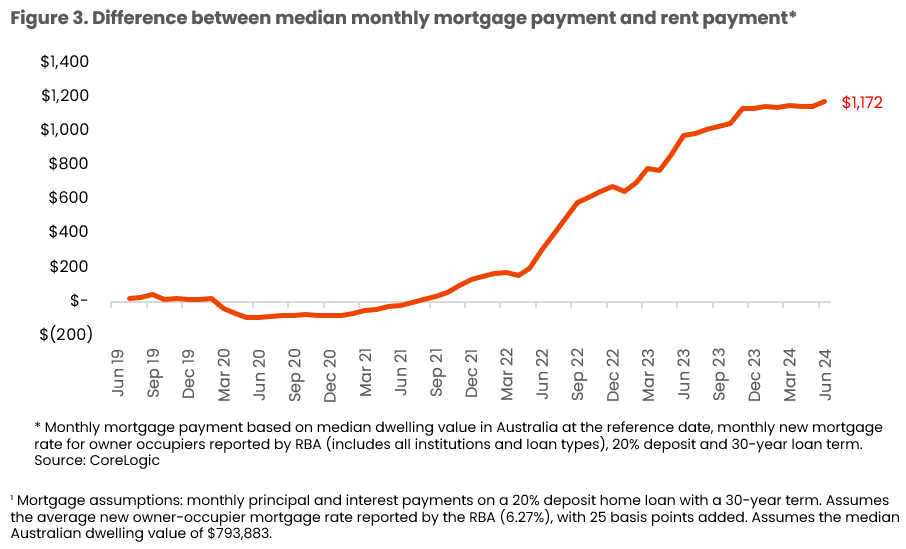

This chart demonstrates the median monthly mortgage payment in Australia now exceeds rent by $1,172 as of June 2024, highlighting a growing affordability gap. The increase is driven by rising interest rates and higher dwelling values, according to CoreLogic data.

Residential mortgage credit rose from $2.185 trillion in September 2023 to $2.288 trillion in September 2024, reflecting robust demand for housing finance. This growth occurred even as borrowers faced elevated costs of borrowing, underscoring the market’s adaptability and strength.

The expansion in mortgage credit was driven by both owner-occupiers and property investors:

This balanced growth indicates sustained confidence in the Australian property market, with both segments contributing significantly to the rise in credit.

APRA emphasized that the overall quality of lending remains sound despite the challenging economic environment. High-risk lending, including loans with high loan-to-value ratios (LVR) and high debt-to-income ratios, remained low and stable:

Meanwhile, the average debt-to-income ratio of borrowers improved marginally, declining from 5.7 to 5.6. These trends indicate that while borrowing conditions have tightened, lenders are maintaining responsible lending practices to manage risks effectively.

The report noted a slight increase in non-performing loans and loans past due, though these remain at manageable levels:

Despite these increases, the overall stability of the lending market suggests that borrowers are largely coping with the pressures of higher interest rates.

New residential loans funded during the September quarter also saw strong growth, rising by 9.3% year-on-year. The value of new loans increased from $150.9 billion to $165 billion, reflecting continued demand for housing finance:

This trend indicates a shift in market dynamics, with investors taking advantage of opportunities despite the higher cost of borrowing.

The commercial property sector mirrored the positive trends in residential lending, achieving significant growth:

APRA attributed this growth to strong demand in the industrial property sector and a resurgence in the retail property sector, both of which contributed to the rise in commercial lending activity.

The continued growth in mortgage credit highlights the resilience of Australia’s housing market and lending institutions. Despite higher borrowing costs, demand for property remains strong, driven by both owner-occupiers and investors. The increase in new loan funding, alongside steady loan quality, underscores the adaptability of the Australian mortgage market.

APRA’s findings also suggest that lenders are striking a balance between expanding credit and maintaining sound lending practices. The slight rise in overdue and non-performing loans signals challenges but does not overshadow the broader growth trajectory.

With mortgage credit on the rise, now is the perfect time to secure a competitive loan. At OM Financial Services, our expert brokers work with over 50 banks to find the best mortgage options that suit your needs.

Reach out today to get the right advice and the best mortgage deal available. Let us help you navigate the market and make the right financial choice for your future.

17 Dec 2024, 12:00 AM

16 Dec 2024, 12:00 AM

12 Dec 2024, 12:00 AM

10 Dec 2024, 12:00 AM

10 Dec 2024, 12:00 AM

At OM Financial Services, our experienced group of contract brokers can compare a wide extent of domestic credits over a board of 50+ banks. This means we won’t use any ancient arrangements for you. We will find the best current arrangement to meet your needs. Our fund masters are talented in taking care of advances, from domestic credit to individual credit, right through asset and commercial finance. We can assist you get advance pre-approval and can give master help for borrowers looking to renegotiate. With OM Financial Services, you’ll have access to comprehensive choices to help assist you with borrowing.